Horse Racing Bankroll Management: Staking Plans That Survive a Losing Run

html

Contents

Why staking matters as much as selection

I spent the first two years of serious punting convinced that finding winners was the whole game. I was wrong. My selections were solid — strike rate around 22% at average odds of 7/2 — and yet my bank barely moved. The problem wasn’t the horses. It was the staking. Some months I’d overbet on “certainties” that lost, then underbet through the next profitable run out of fear. The selection edge existed; I was just throwing it away with undisciplined money management.

Staking is the mechanism that converts a theoretical edge into real-world profit. Without it, even a punter with genuine skill in reading UK racing form can flatline or go broke. Ten percent of the UK adult population participates in online sports betting, and only a fraction of those bettors apply any formal bankroll structure. The ones who survive are not necessarily the best form readers — they are the best money managers.

Sizing your starting bank

The number everyone asks first: how much money do I need? The answer depends on two things — your expected strike rate and your tolerance for volatility. A bank needs to be large enough to withstand the longest plausible losing run without being wiped out, while still allowing individual stakes that are meaningful enough to matter when winners land.

For a punter backing selections at average odds of 3/1 to 5/1, a starting bank of 50 to 100 points is a reasonable foundation. A “point” is your standard stake unit. If your comfortable unit stake is 20 pounds, a 50-point bank means 1,000 pounds set aside exclusively for betting. That money should be entirely separate from household bills, savings, and discretionary spending. If you cannot comfortably lose it, the bank is too large, and the psychological pressure will compromise your decision-making long before the maths catches up.

I started with a 60-point bank and worked up. The key is that the bank is a fixed number you protect, not an open-ended pool you dip into whenever a fancied runner appears. If the bank halves, you halve the unit stake. If it grows, you can scale up gradually. The discipline is non-negotiable.

Level stakes, percentage and Kelly fraction

Three staking methods dominate serious punting, and each suits a different temperament and skill level.

Level stakes is the simplest. Every bet gets the same stake — one point per selection, no variation. The advantage is total clarity: your results reflect your selection ability directly, without staking distortion. The disadvantage is that you stake the same amount on a strong 20% edge as on a marginal 2% edge, which leaves profit on the table. I recommend level stakes for the first six months of disciplined betting, because it forces you to evaluate your raw form-reading skill before adding staking complexity.

Percentage staking adjusts each bet to a fixed percentage of the current bank — typically 1% to 3%. As the bank grows, stakes grow. As it shrinks, stakes shrink automatically. This self-correcting mechanism makes it almost impossible to bust a bank entirely, which is its main attraction. The drawback is emotional: after a losing run your stakes become small, and the recovery curve feels painfully slow.

Kelly criterion is the theoretical optimum. It calculates the stake as a proportion of your edge relative to the odds. The formula is (bp minus q) divided by b, where b is the decimal odds minus one, p is your estimated probability of winning, and q is one minus p. Full Kelly is famously aggressive — a single bad probability estimate can lead to wild overexposure. Most professional punters use a fraction, typically quarter-Kelly or half-Kelly, which sacrifices some theoretical growth rate for substantially lower variance.

Nearly a quarter of respondents in a recent punting survey had been subjected to affordability checks, and 61% refused to hand over financial documents. For punters operating under regulatory scrutiny, fractional Kelly with smaller absolute stakes can help stay below the radar of automated triggers while still applying disciplined staking principles.

The maths of a normal losing run

Every punter experiences losing streaks. The question is not whether they will happen but how long they will last and whether your bank can absorb them. This is where most recreational bettors panic and abandon their system — precisely the moment discipline matters most.

A punter with a 20% strike rate will, on average, experience a run of 15 or more consecutive losers at some point across 500 bets. That is not bad luck — it is statistical normality. If your unit stake is one point and you hit a 15-bet losing streak, you need 15 points of bank to survive it. A 50-point bank absorbs that comfortably. A 20-point bank does not.

Nevin Truesdale, the former Jockey Club chief executive, warned that many of the consequences racing feared from tighter regulation are materialising, observing that blanket checks show no discernible impact on problem gambling levels while significantly damaging racing’s finances. For the individual punter, the parallel is clear: external constraints on your activity — account restrictions, affordability interventions — can hit during a losing streak when your bank is already under stress. Building a bank that tolerates extended downswings is as much about regulatory resilience as it is about statistical survival.

I keep a simple rule: if my bank drops to 40% of its starting level, I stop for a week, review my last 50 bets, and assess whether the drawdown reflects bad variance or bad selections. If the process was sound and the edge estimates hold up historically, I continue at a reduced unit stake. If the process was flawed, I fix the inputs before placing another bet.

Discipline rules for protecting the bank

Rules only work if you follow them when they hurt. Here are the five I’ve used for the last seven years, written on a card that sits next to my monitor.

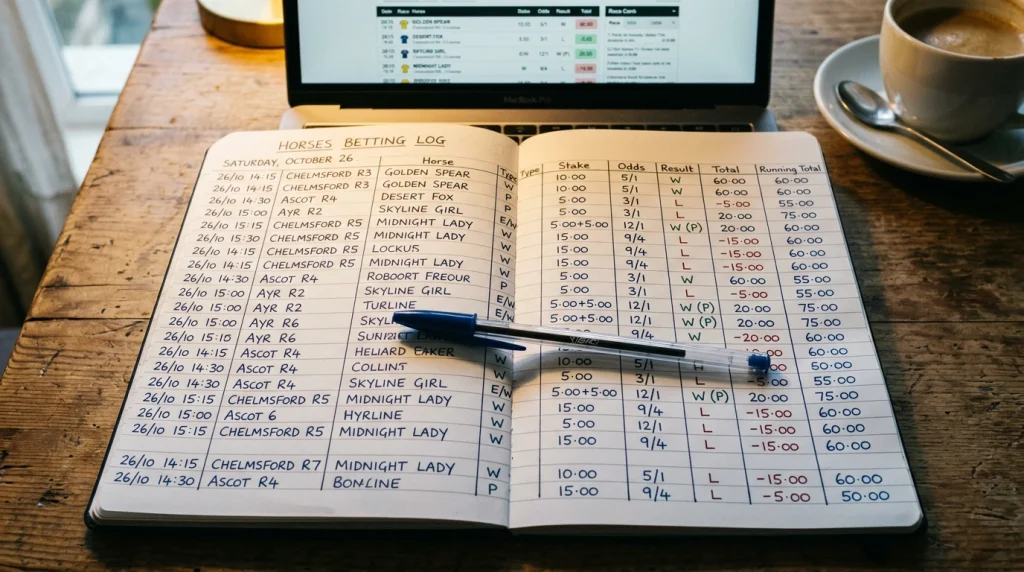

Never stake more than 3% of the current bank on a single bet, regardless of confidence. The race you feel most certain about is often the one where blind spots hide. Second, never increase stakes to recover a loss — chasing is the fastest route to bank destruction and the hardest impulse to suppress. Third, record every bet before the race, including your estimated probability and the price taken. Post-race rationalisation is worthless; pre-race documentation is evidence. Fourth, review staking performance monthly, not daily. Daily reviews amplify noise and encourage reactive changes. Monthly reviews reveal patterns. Fifth, keep the betting bank in a separate account — not in your main current account where it blends with rent money and takeaway orders.

These rules are not complicated. They are not secret. The difficulty is executing them consistently through the emotional noise of a losing Saturday or the euphoria of a winning week. The punters who build lasting banks are the ones who treat staking as a system with rules, not a series of individual gut decisions linked to how strongly they rate each value selection.